How does Altruist generate revenue? We get this question a lot and we’re happy to be transparent about it.

Altruist is a “self-clearing custodian.” That means we are a broker-dealer that handles the submission and settlement of trades. In other words, we manage both the front end and back end of the trading process. This allows us to make quicker service adjustments and enables us to deliver a better, more positive client experience.

In this dual capability, Altruist generates revenue in a variety of ways. We’ve listed them below, in no particular order. Note that the weight of these revenues is dependent on market conditions and macro factors, as well as the assets managed by advisors.

1. Interest on cash deposits

Altruist earns interest on the cash deposits held in client accounts by sweeping uninvested cash to FDIC-insured partner banks. We earn the spread between what our partner banks pay and what is paid out to clients. This practice requires balancing profitability for the business with providing competitive interest rates for clients.

In line with our mission to make financial advice better, more accessible, and more affordable, we’ve prioritized account offerings that deliver exceptional value. When Altruist advisors requested a high yield cash option for clients, we delivered Altruist Cash, which offers a yield 11 times the national average.* Altruist advisors can now offer an industry-leading APY to clients, ensuring they’re getting the most out of their cash.

2. Margin interest

Margin is not yet available on Altruist, but it will be a source of revenue in the future. When clients buy securities on margin, Altruist will lend the funds, charging interest on the borrowed amount. It’s important that rates remain reasonable and clients are aware of the associated risks.

3. Fully paid securities lending

Altruist offers fully paid securities lending, a practice that involves lending out securities owned outright by clients to other traders or institutions. We earn lending fees from this service, while the borrower provides collateral and pays interest.

Clients benefit by receiving a portion of the lending fees, providing them with an additional source of income on their fully paid securities. Additionally, clients retain 100% ownership of their assets, which can be sold at any time. Of course, clients should be aware of the risks associated with any securities lending program before participating.

4. Payment for order flow

As a self-clearing custodian, Altruist receives compensation for market orders that we handle. This fee is relatively small and generates revenue based on trade volume.

Although the practice is common, advisors should consider how payment for order flow (PFOF) could potentially impact execution prices, and understand how their custodian handles trade execution and PFOF.

Altruist prioritizes three key principles when executing orders:

Speed: Milliseconds matter, and our fast trades ensure customer orders get the best available price.

Routing Optimization: Our routing system directs orders via numerous thoroughly-vetted market makers to ensure the most desirable execution.

Price Improvement: Our team regularly looks for ways to improve prices, passing savings on to clients.

Ultimately, PFOF is only a minor revenue source for Altruist, and our profit margin comes from sending orders to the best venues. You can learn more about our execution quality and philosophy here.

5. Revenue share agreements with mutual funds (12b-1 fees)

We have agreements with mutual fund companies, earning a portion of the 12b-1 fees charged by these funds for marketing and distribution expenses. However, Altruist also offers the largest selection of No-Transaction-Fee (NTF) mutual funds – allowing clients to invest in a wide range of diversified funds while avoiding extra fees.

6. Ticket charges and trading fees

Altruist charges fees for processing trades or transactions, known as ticket charges, along with certain other types of trading fees. Our philosophy is that these fees should be easy to understand, and as good – or better – than the most competitive legacy alternatives.

Altruist advisors can offer clients competitive fees on activity like ACH transfers and mutual fund transactions, as well as provide commission-free trading (including fractional shares) of individual securities, ETFs, and warrants.

On top of being simple and competitive, fees should always be transparent. You can see the Altruist Financial fee schedule here.

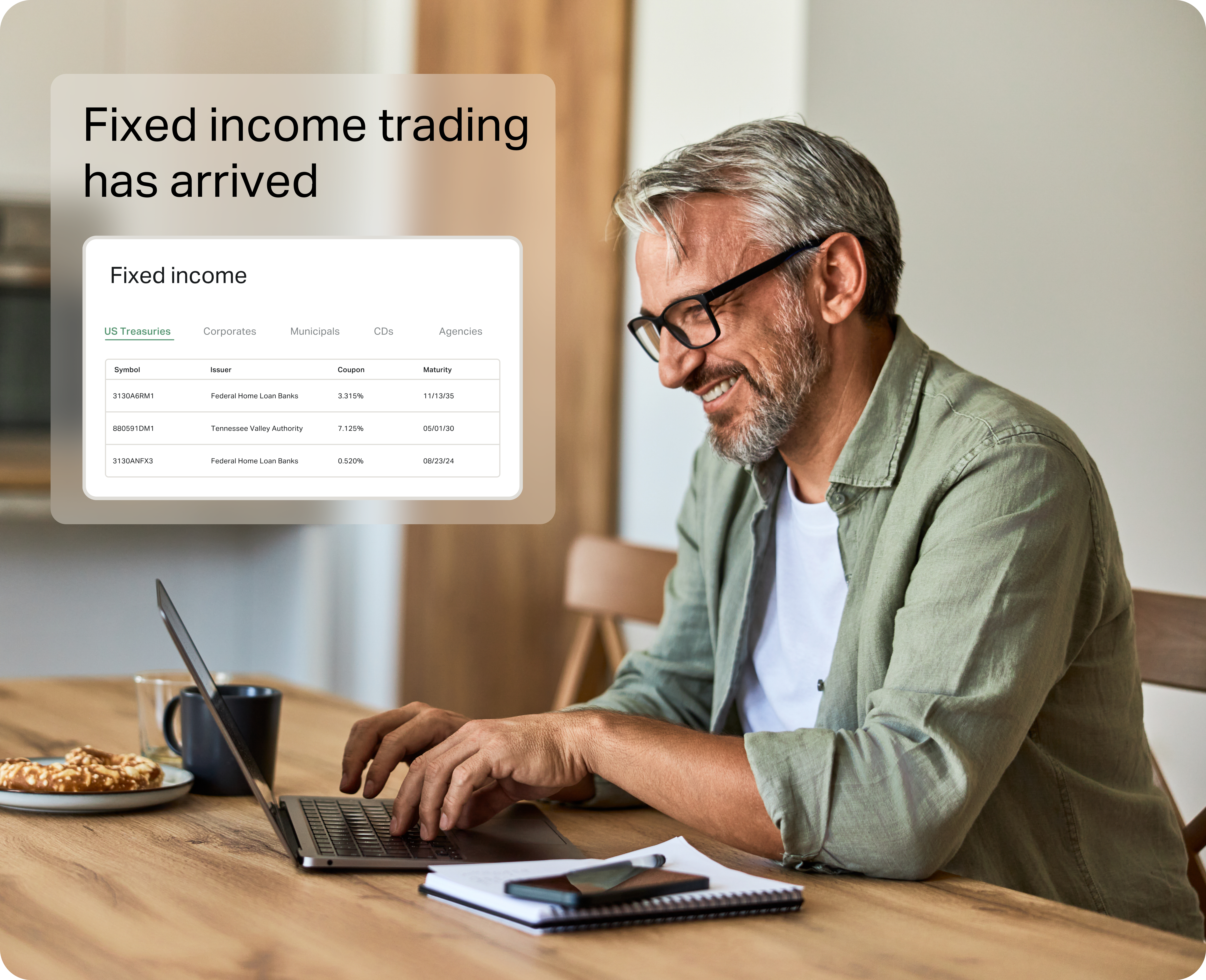

7. Technology

Finally, Altruist generates revenue through fees for certain integrated tools and technology. This includes our model marketplace, which offers over 350 different models covering a wide range of strategies at industry-low cost, and TaxIQ, our new suite of tax management tools. TaxIQ automates key practices like tax loss harvesting (TLH), gain deferrals, and wash sale awareness to ensure client portfolios are maximally tax-efficient.

What Altruist does not charge for

In discussing the ways Altruist generates revenue, it’s also worth noting the ways we don’t. Building a world with better financial advice begins by offering advisors the tools to succeed at reasonable or no cost – and our pricing decisions reflect that.

For example, we’ve zeroed out the portfolio accounting software expense for all Altruist brokerage accounts. Advisors who custody with Altruist receive built-in performance reporting, fee billing, portfolio rebalancing, a modern client portal, and portfolio accounting at no additional cost.

This pricing sits in stark contrast with existing options; for most advisors, portfolio accounting software is the most expensive part of their tech stack. According to Michael Kitces, advisors are spending between $40 to $70 per account per year.

We take a similar approach to trading, administrative, and cashiering fees. Our streamlined fee schedule allows advisors to offer clients zero commissions when trading equities, ETFs, warrants, and treasuries. Partial ACAT transfers, Roth conversions, 401(k) plan administration, and corrected tax forms all come with zero fees.

What this means for financial advice

Enabling advisors to deliver great outcomes for clients is our top priority, and that requires providing maximum value while charging minimal fees. We're confident that this model will prove superior in the long run, allowing more people to access quality financial advice at a reasonable cost.