As Altruist’s COO, my primary responsibility is to ensure that we remain a strong, stable, and secure custodian. Over the course of hundreds of conversations with advisors considering a switch to Altruist, they justifiably ask: “Is my clients’ money safe?” This is a great question and an essential part of due diligence. The article below is the answer I often give (granted, a bit longer) when I have those conversations.

—

What does a custodian do?

A custodian’s job is to safeguard client assets, process account-based actions (e.g., opening an account, transferring funds, purchasing or selling securities, adding or updating beneficiaries, etc.), and stay compliant. This responsibility is entrusted only to institutions with a proven ability to maintain a complex technical architecture and withstand rigorous, ongoing scrutiny from a longstanding network of taxpayer-funded regulatory agencies.

In the U.S., all custodians are regulated by the SEC, FINRA, DTCC, and 53 states and territories. This level of oversight explains why new custodians aren’t popping up every couple of months.

Protecting client assets

All advisors should be aware of the SEC’s Customer Protection Rule—Rule 15c3-3. This 50-page rule protects clients by mandating that all custodians keep client assets completely segregated from company funds, guarding those assets against potential misuse. It is a very good and important rule.

Also worth calling out is that all custodians clear assets through the Depository Trust and Clearing Corporation (DTCC). When you put money into a client account or buy securities on their behalf, those assets sit in a “digital box” at the DTCC in New Jersey. That’s the case whether you’re at Schwab, Fidelity, or Altruist. All that changes when you switch custodians is the box number and the firm responsible for the accounting of that box.

Insurance

All custodians carry insurance, including membership in the Securities Investor Protection Corporation (SIPC), errors and omissions (E&O) insurance, and fidelity bonds. Schwab, Fidelity, and Altruist also carry excess SIPC insurance policies.

SIPC and excess SIPC provide protection when businesses misuse funds or engage in fraudulent practices. For example, you may have a broker-dealer who's got a hedge fund business, an advisory business, and an underwriting business—they may even be running public funds. If one of those business units, due to some sort of macro-condition, starts running into trouble, they might start dipping into other business units or drawing on funds that they shouldn't have, doing things that they're not supposed to. If something precipitates an event whereby they're unable to meet their obligations, that's where SIPC comes in.

If you’re only an RIA custodian, and you’re following Rule 15c3-3, this point is largely moot. Altruist carries $150 million in excess SIPC insurance; Schwab carries $600 million in an excess SIPC policy. (Custodians carry excess SIPC policies in de minimis amounts relative to the amount of assets we’re actually custodying because we’re focused on 15c3-3 compliance.)

Asset Protection Guarantees

Like Schwab and Fidelity, if a client ever loses money in an Altruist account due to unauthorized activity, we cover that loss 100%. (Note: some basic security feature usage is required and this does not apply to market losses. To learn more about the guarantee, Altruist provides additional information here).

This strict set of safeguards—in an already meticulously monitored and highly regulated financial system—ensures that custodians are not only capable of protecting client assets but are, in fact, doing so. Altruist takes these regulations very seriously, and reports indicating our compliance are available at adviserinfo.sec.gov.

Why over 4,000 advisors choose Altruist

While this regulation and functionality connect all custodians serving RIAs, there are also significant ways in which custodians vary. Below I’d like to explain why many advisors choose to custody client assets with Altruist over legacy incumbents.

Modern technology and security

Altruist’s platform isn’t burdened by the technical debt of on-premise systems. Advisors and clients benefit from the most contemporary cybersecurity features, with automation and digitization built into nearly every workflow. This not only reduces the risk of operational errors and fraudulent activity but frees up time for the more meaningful parts of the advisor-client relationship.

Better client outcomes and experiences

Our (ambitious) goal is to empower advisors to generate 150 bps in improved outcomes for their clients. To that end, we offer things like fractional shares, which help minimize tax drag, built-in tax loss harvesting features to help automate client tax savings, and a high-yield cash account with an industry-leading APY. Where legacy custodians are still relying on paper forms and outdated client portals, our client mobile app provides a retail-quality experience within an advisor-mediated offering.

Lower costs

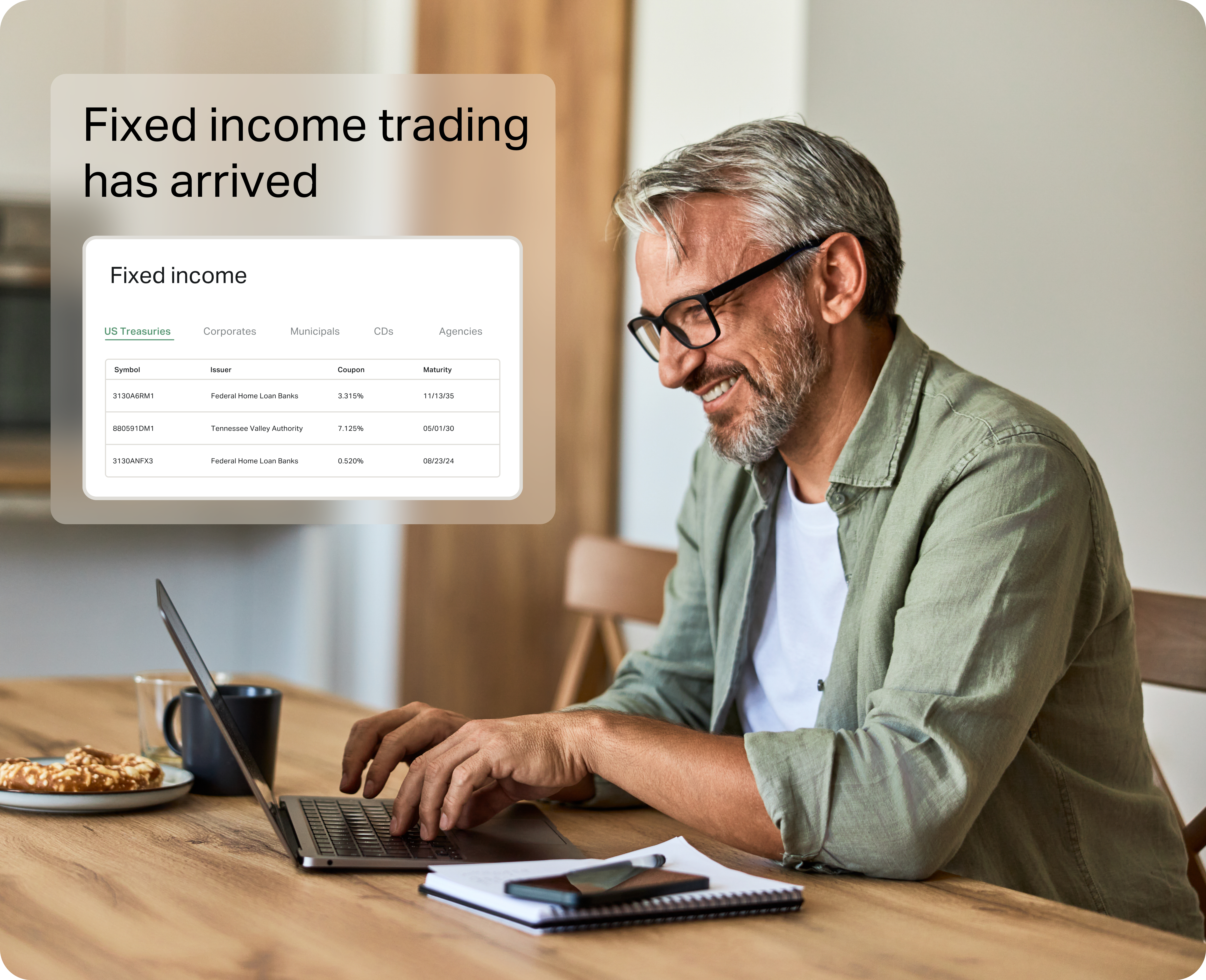

At Altruist, there are no AUM minimums, platform fees, or hidden costs. Advisors get PAS and fee billing for free with all Altruist brokerage accounts, and we offer commission-free trading on ETFs, individual securities, and warrants alongside one of the largest NTF (No Transaction Fee) lists. When it comes to bond trading, our fees are among the lowest in the industry. By keeping costs low and maintaining a simple, transparent, and highly competitive fee schedule, advisors are empowered to build more cost-efficient portfolios. You can learn more about our pricing philosophy here (and if you want a clearer picture of how Altruist makes money, you can review that information here).

Built to serve RIAs

Unlike other custodians, we don’t have a competing retail business. That means our entire focus is on helping advisors do their best work, whether that’s through building powerful technology, co-creating our product with our customers via our Idea Portal, or offering reliable, highly-trained support. Advisors deserve a custodian that can act as a partner, not just a vendor.

—

In 2022, Vanguard refreshed its longstanding Advisor Alpha study¹, showing how advisors can add as much as 3% in net returns annually through strategies like behavioral coaching, tax-efficient investing, and disciplined rebalancing—services that clients simply don’t get through DIY platforms.

At Altruist, we have always known that advisors are a significant differentiating factor in building and preserving wealth. For clients, choosing the right financial advisor is critical. For advisors, the same is true of choosing a custodian.