When it comes to performance, there’s really only one number that matters to your clients: their after-tax, after-fee, take-home return.

These are the only dollars available when it comes time for a client to spend their hard-earned savings. Since taxes can produce significant drag on take-home returns, active tax management can help your clients keep more of what their portfolio has earned.

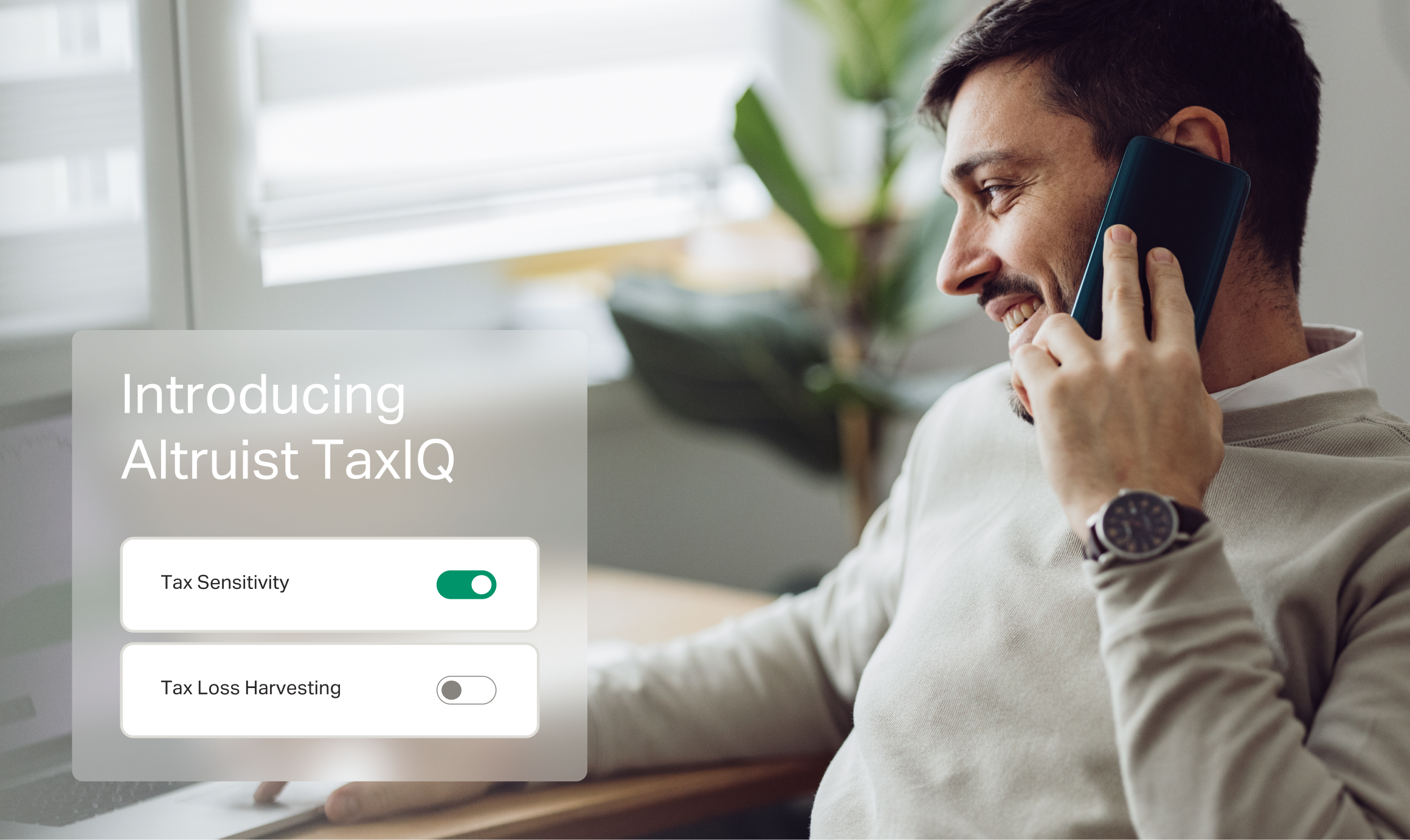

Altruist is proud to announce the launch of TaxIQ, our forthcoming suite of automated tax management capabilities.

Studies on performance contributions from institutions like Vanguard, Morningstar, Smartleaf, Envestnet, Russell, and others indicate that tax management is second only to behavioral tendencies when it comes to long-term influences on investor performance. Active tax management can even help improve investor behavior–especially in down markets–which we’ll explore later.

Performance contribution

Literature review

Because tax management is complicated, we’ll break down the big questions so you can evaluate these new, powerful tools. Mainly:

- What is tax management and how do I explain it to my clients?

- What are the benefits of tax management?

- How does this functionality work within the Altruist platform?

- Which clients are a good fit for these tools?

Tax management explained

Broadly speaking, tax management is a set of investment strategies that help reduce a client’s total tax burden.

This includes gains deferrals, tax loss harvesting, wash sale avoidance, gains budgeting, asset location, lot selection, and tax efficient product selection. Taken together, these strategies can generate a substantial amount of tax alpha.

Simply put, by taking a strategic approach to when, where, and what an advisor buys and sells on behalf of his or her clients, significant tax savings can be achieved.

How significant? The answer is almost always, “it depends”, but many academic and practitioner studies suggest after-tax performance benefits tend to range between 1% and 2% of additional annualized return for some investors (Bouchey, 2016, WSJ, 2021, Vanguard, 2022).

Behavioral benefit: Generate value in down markets

What’s more, tax management can be especially potent during down markets. When markets are down, tax opportunities increase, especially those related to tax loss harvesting. This means you are doing more for your clients at exactly the time when clients may be most concerned about their portfolios.

Being able to highlight the value you’re adding to their after-tax returns can help assuage client concerns during downturns and help them stay committed to their investment plan in times that may feel particularly challenging to do so.

Sophisticated tax strategies in significantly less time

Tax strategies can help differentiate your practice, but typically they come at a cost–in the form of time-intensive work for you.

Fortunately, TaxIQ automated implementations on the Altruist platform allow you to pursue tax alpha on behalf of clients without managing individual positions, selecting tax lots, or timing trades.

With a simple toggle, advisors can enable two critical features at the account level: 1) tax sensitivity, which gives an added level of tax awareness to the automated rebalancer, and 2) tax loss harvesting.

How the Altruist TaxIQ suite works

Tax Sensitivity

Tax Sensitivity works by making smart tradeoffs between tax impact and tracking of the portfolio’s target allocation. Specifically, Tax Sensitivity enables:

- Gains deferral. Tax Sensitivity tends to avoid selling securities at a gain if the portfolio is within its specified drift thresholds. For example, when investing a deposit, the rebalancer will seek to buy underweight securities and be more cautious about selling overweight securities. Generally, it will seek to sell overweight securities with no embedded gains since there is no additional tax impact. For positions with embedded gains, it will carefully trade off the benefit of realizing gains versus reducing drift from the target portfolio.

Deferring short-term realized gains is particularly useful, since these gains are generally taxed at a higher rate. Tax Sensitivity considers the tax impact of realizing short-term versus long-term capital gains. By default, Tax Sensitivity seeks out the least expensive tax lots to sell by considering the size of the gain or loss, the term for which each lot has been held, and the difference between long- and short-term tax rates.

- Wash sale awareness. Tax Sensitivity seeks to protect realized losses from wash sales. Even without TLH turned on, you may generate realized losses in a portfolio, either through the regular course of rebalancing or from manual tax loss harvesting. Given the value realized losses have to reduce tax liability, we want to avoid washing losses with subsequent trading activity when possible. Wash sale awareness keeps track of trades in the client’s account at the tax-lot level and seeks to avoid transactions that wash a recently realized loss.

Tax Loss Harvesting (TLH)

Tax loss harvesting means selling securities at a loss to realize, or “harvest,” a capital loss. The realized loss can be used to offset capital gains, whether or not the gains are in the same account or have been realized elsewhere. If there are additional realized losses after netting against gains, those losses can offset up to $3,000 of taxable income. Any remaining losses can be carried over to be used in subsequent tax years.

If Altruist’s Tax Loss Harvesting is enabled for a client account, the rebalancer will seek to harvest losses when a rebalance is triggered. Proceeds of sales are invested in other securities in the portfolio, including fund substitutes when designated, to help maintain market exposure while seeking to avoid wash sales.

Tax loss harvesting is part of a holistic rebalancing process at Altruist. This means portfolio drift from target allocations is considered when evaluating harvesting opportunities. When there is sufficient harvesting opportunity, rebalancing may introduce further drift from target weights, while generally staying within predefined drift boundaries, without sacrificing pre-tax returns. In other cases, tax loss harvesting can help reduce drift by using the proceeds of harvest sales to buy underweight securities.

Loss Threshold

A natural question is when should one choose to sell a security at a loss? Sell too soon and you may miss the opportunity to harvest a larger loss. Wait, and risk the price rebounding and missing the harvest opportunity.

Altruist’s Tax Loss Harvesting considers these competing risks. Loss thresholds are determined by the overall volatility of the security. Intuitively, if a short-term bond fund is down by 5%, that's a relatively big move and may represent a good opportunity to harvest. For a small-cap stock, on the other hand, a 5% drawdown may not be unusual, and harvesting at this point may leave the potential for a larger harvest on the table.

Loss thresholds also get more aggressive, ie: harvesting occurs for smaller losses, as we come closer to the end of the tax year. Since a loss in January can’t be applied to gains in the previous year, we seek to harvest more losses, even if smaller, before the start of a new tax year.

Altruist Tax Loss Harvesting also evaluates if a loss will be treated as short or long-term. If a short-term lot held at a loss is approaching long-term status, the rebalancer will be more eager to realize the loss so it can be available to offset (more heavily taxed) short-term gains.

Reinvestment of proceeds

The proceeds of tax loss harvest sales are used to help reduce expected tracking to the target portfolio. This is achieved by purchasing securities in the portfolio that are correlated to the security that was harvested. For example, if Microsoft was sold, the proceeds may be used to buy other large-cap technology stocks that are in the target portfolio. The proceeds may also go towards purchasing other underweight securities in the portfolio.

For mutual funds and ETFs, you can designate fund substitutes. A fund substitute will be treated as a roughly equivalent replacement for the fund that was sold. All things equal, the proceeds of the sale of a fund will be used to buy the fund substitute if one is designated. Fund substitutes allow for more control over what may be purchased when a harvest takes place and is considered a best practice when tax loss harvesting with funds.

Fund substitutes may allow for a more effective tax loss harvesting program. Because fund substitutes are treated as equivalent to the primary security, positions at a loss can be fully liquidated and replaced with the substitute, allowing the full loss to be captured.

Wash sales

Altruist’s Tax Loss Harvesting tracks sales at the tax-lot level. When TLH is on in an account, all rebalancing activity–whether harvesting a loss, reducing drift, or managing cash flows–seeks to minimize wash sales in the account.

Who is a good fit? Some considerations

TaxIQ will only be available in taxable accounts. When it comes to specific clients and accounts, as a rule of thumb for tax-loss harvesting, start with your clients who have capital gains in their portfolios or elsewhere that could be offset by harvesting the loss. If they fall into one of the higher tax brackets, they may stand to benefit the most from a tax loss harvesting strategy.

Another sign that your client could be a good candidate for tax-loss harvesting would be instances where a tax liability was generated from a large sale of real estate or a business.

One note of caution: if the client’s tax rate will be increasing in the future, you may need to be careful–harvesting losses now could cause them to pay more for those deferred taxes in the future than if they paid them today.

While not an exhaustive list of considerations, we’re excited to make tax loss harvesting easy to implement for any client on the Altruist platform.

What’s next on the Altruist TaxIQ tax management roadmap?

We’re always working to deliver better outcomes for you and your clients.

In the near future, we’re enhancing our reporting functionality and implementing a gains budget tool for even greater control over your clients’ tax liabilities. We’re also adding a new rebalance method to check accounts for loss harvesting opportunities daily. Want to join the discussion? Sign up for Altruist and connect with our team in Altruist’s Idea Portal.

Already on Altruist? Start to prepare your accounts for making use of TaxIQ by reviewing our best practices knowledge base article in our Help Center (log in to access). TaxIQ will be made available to all advisors on Altruist at the end of June.

If you’d like to learn more, please get in touch with us.