This post is brought to you in partnership with Liberty Street Advisors.

Today's investors are closely examining how economic trends, interest rates, and geopolitical factors will influence their portfolios. This scrutiny has prompted a shift towards strategies that balance the minimization of volatility with the optimization of risk-adjusted returns. The expansion of private market offerings now provides a diverse array of investment opportunities tailored to individual risk, return, and liquidity preferences, leading to a surge in alternative investment allocations. This trend is expected to propel private market assets under management to exceed USD $18 trillion within five years, according to Preqin, encompassing areas like private equity, venture capital, real estate, infrastructure, and credit.

The venture capital (VC) sector in 2023 mirrored the previous year, marked by slower capital deployment rates, compressed valuations, and subdued exit opportunities. Despite the lack of direct correlation between public and private markets, investor sentiment can significantly affect the latter, especially during downturns, due to challenges such as reduced transparency, liquidity, and information asymmetry. Consequently, the private market is becoming divided, with high-performing assets attracting rewards and less successful, cash-strapped entities facing hurdles. In such times, discerning investors often apply stricter discipline and seek to capitalize on market dislocations.

While the current market difficulties are considerable, the investment team managing The Private Shares Fund, The Private Shares Group (PSG), has persisted in investing through this cycle with a cautious approach. Focusing on late-stage VC-backed firms, the team selects companies with solid operating metrics, differentiated business models, strong financial foundations, experienced management, and reputable investor groups. PSG prioritizes sectors poised for rapid growth, such as the Space Economy, Artificial Intelligence/Machine Learning, Cyber Security, Robotics/Hardtech, Big Data/Analytics, Fintech, Digital Health, among others.

PSG maintains that the VC sector will remain a key driver of private innovation globally. Historical patterns suggest that dislocated periods can offer appealing opportunities that lead to outperformance in the following years. However, such investment strategies require a long-term view to potentially reap the rewards of capital growth and exit value creation.

Secondaries

Explaining 'secondaries' and 'secondary transactions' sheds light on their significance in private markets. Unlike their public counterparts, private markets lack a centralized exchange for trading assets, making them inherently illiquid. This limitation applies whether dealing with fund interests, company securities, or complex deal structures. However, a growing secondary market, with over $100 billion in annual transactions, offers liquidity for these assets, despite being less efficient and transparent than public markets. In this context, 'secondaries' refer to the investment strategy focused on this market, and 'secondary transactions' are the deals executed within it. Sellers gain the opportunity to liquidate assets, while buyers can benefit from discounted prices, reduced holding periods, and diversification across vintage years. Complex deals may also allow fund managers or companies to secure liquidity, new capital, and extended time for asset exits.

PSG offers insights into the secondary market's state from a perspective keen on direct company securities. PSG emphasizes a long-term investment horizon, advising patience and discipline for investors looking to capitalize on such strategies.

Discount To 'Last Funding Round'

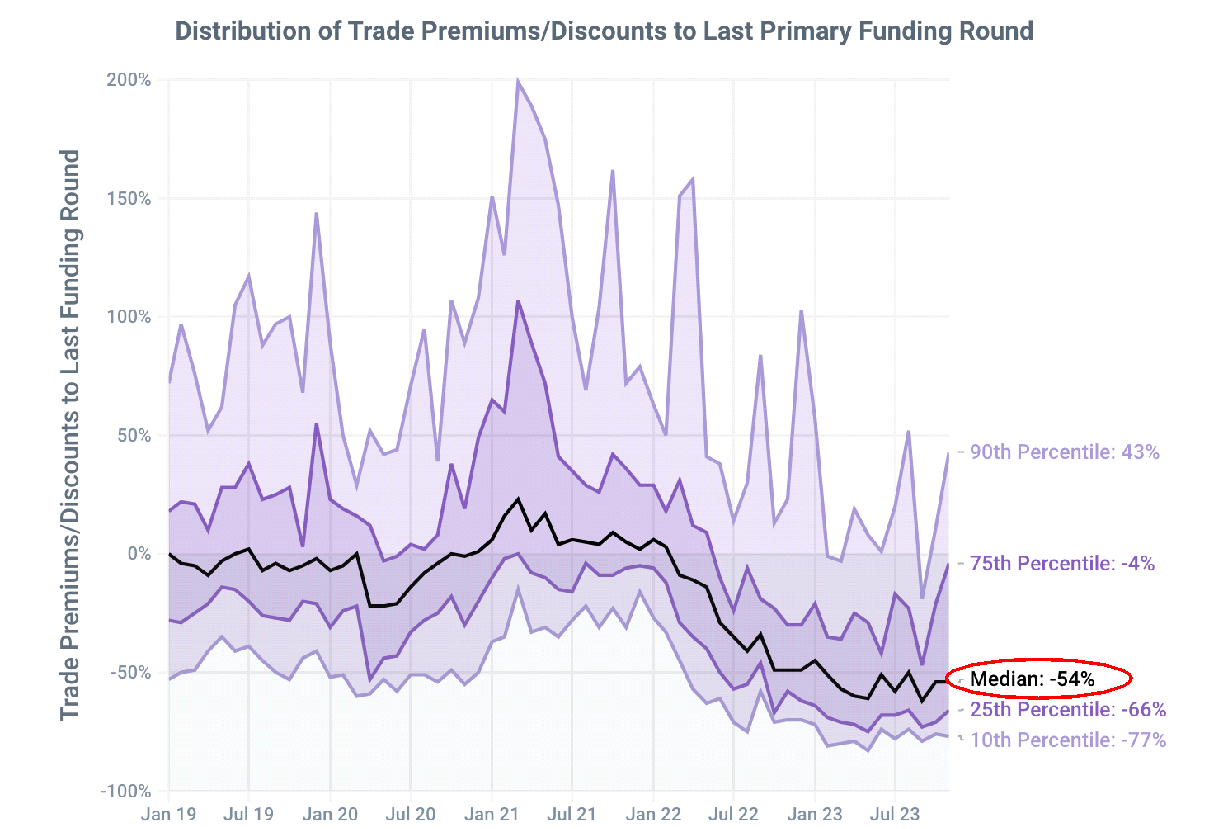

Recent macroeconomic shifts have disrupted the supply-demand balance in VC deal-making, creating an inventory surplus and misaligning seller expectations with buyer demand. This imbalance has broadened the price range for secondary venture-backed company shares, transitioning from a seller's market in 2020/2021 to a buyer's market in 2022/2023. This shift has endowed active investors with greater negotiating power, leading to more favorable terms and significant discounts relative to the last funding rounds.

A chart from Forge, analyzing pricing trends up to November 2023, indicates a 54% discount from the most recent funding round, aligning with transactions conducted by PSG in recent years. This data underscores the evolving dynamics within the secondary market, highlighting the opportunities for informed investors to engage with private market assets under advantageous conditions.

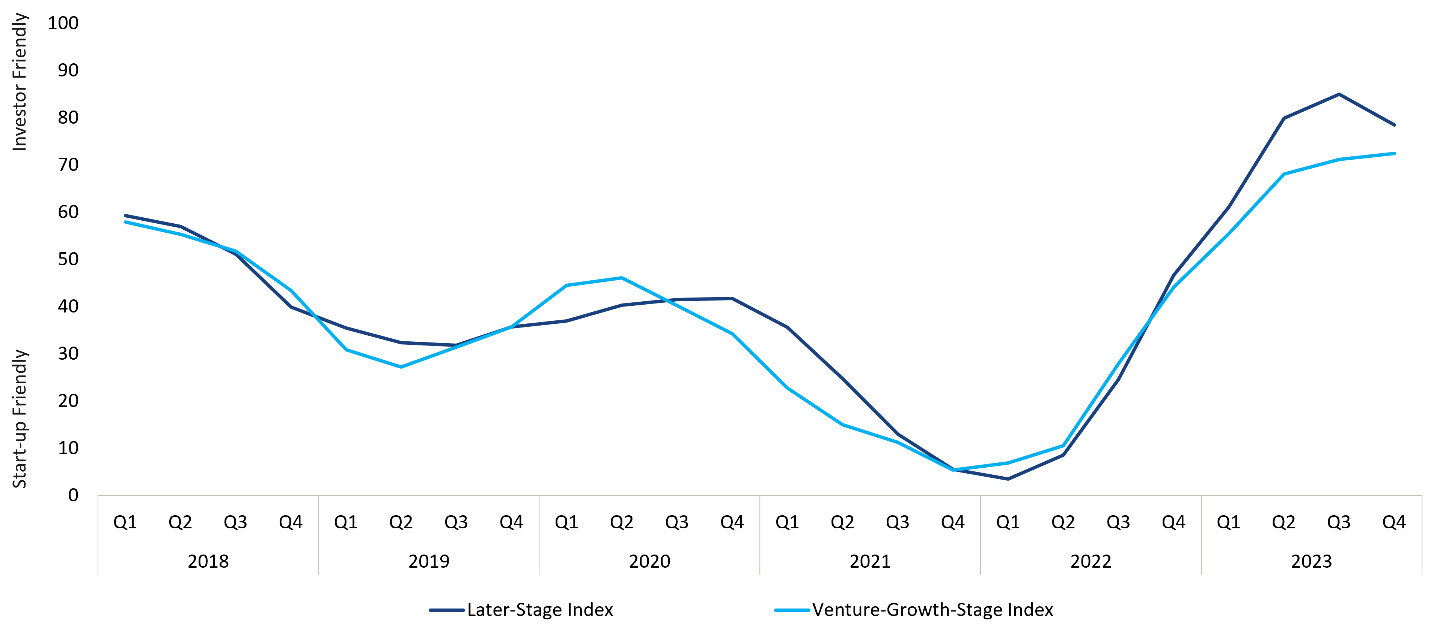

The second chart from Pitchbook's NVCA Venture Monitor for the fourth quarter of 2023 portrays a clear picture of investor sentiment within the venture capital landscape. This period is marked as the most 'investor-friendly' deal environment in more than a decade for both venture-growth and late-stage venture companies. This shift follows a late-2021 period that was notably favorable to startups. The transition to a more 'investor-friendly' climate is observable across all stages of venture capital, with investors gaining leverage to secure more advantageous terms. These terms may include lower company valuations and, in some situations, the negotiation of higher liquidation preferences, warrants, and cumulative dividends.

This change in the deal-making environment reflects a significant shift in the power dynamics between startups and investors. During startup-friendly periods, high demand and competition among investors can lead to higher valuations and more favorable terms for startups. However, as the market shifts towards being more investor-friendly, investors find themselves in a stronger position to dictate terms, leading to potentially lower valuations for startups and more protective provisions for investors. This dynamic underscores the importance of timing and market conditions in venture capital investment strategies, highlighting the need for investors to stay informed and adaptable to capitalize on these shifts.

Pitchbook as of 12/31/23

During times of heightened volatility and uncertainty, markets can present lucrative opportunities for investors with a long-term perspective. This is the rationale behind PSG's continued active capital deployment even amidst challenging conditions. The firm upholds a disciplined approach, engages in thorough due diligence, and utilizes its extensive private market network for exclusive deal sourcing and information gathering.

Right of First Refusal (ROFR)

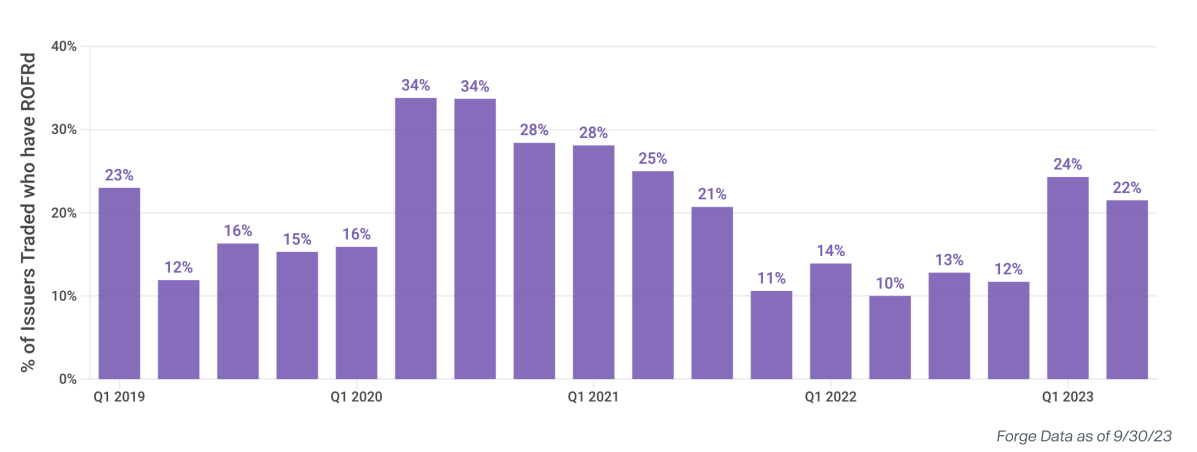

The Right of First Refusal is a clause that allows a company and/or certain shareholders first dibs on buying shares an existing shareholder wishes to sell in a secondary transaction to a buyer where terms have been agreed . If the ROFR holder opts not to buy, the sale to an outside party or existing shareholder that does not have a ROFR can proceed. A rise in ROFR executions could indicate that companies and/or shareholders see the terms as favorable, possibly undervaluing the shares. However, during tough market periods, the focus often shifts towards capital conservation, leading to a higher likelihood of ROFR rights being waived.

Forge's data reveals an interesting trend: venture-backed companies exercised their ROFR rights on average in 34% of secondary deals in the second quarter of 2020, which decreased to 10% by the second quarter of 2022. By the third quarter of 2023, the rate of ROFR execution climbed to 22%, a change PSG is closely observing as a potential indicator of market dynamics shifting. This pattern underscores the strategic considerations companies and shareholders navigate in response to evolving market conditions, balancing investment opportunities against capital preservation priorities.

IPO Market

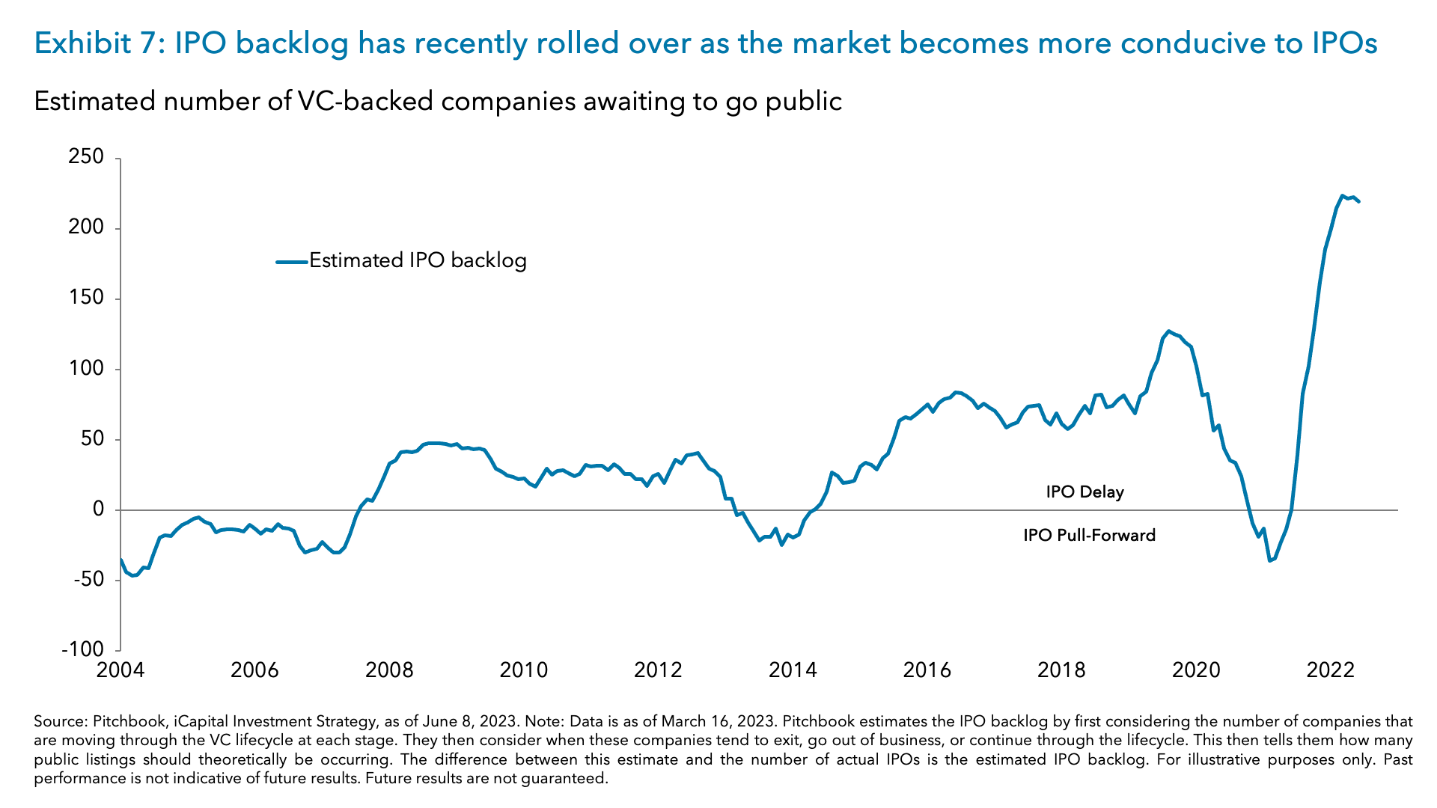

The two most common exit paths for late-stage venture-backed companies are mergers and acquisitions (“M&A”) and public market listings. While direct listings (also known as direct public offerings, or “DPOs”) and special purpose acquisition companies (“SPACs”) became popular in recent years as public listing alternatives to traditional initial public offerings (“IPOs”), the latter will likely continue representing the majority of public listing activity. At present, PSG believes there is a very deep, high-caliber backlog of IPO candidates and sees green shoots developing for 2024, particularly if public and private market sentiment continues improving.

To further support PSG’s view, the chart below from iCapital illustrates an unprecedented backlog of more than 200 venture-backed companies waiting to go public which could lead to a flurry of IPOs in 2024. While this view is also held by several of the Fund’s underlying portfolio companies and co-investors particularly in areas such as artificial intelligence, cybersecurity and fintech, PSG believes such activity depends on a continued strengthening macro environment.

iCapital as of 11/12/23

Summary

In the last two years, PSG has spotted trends hinting at an improving outlook for private markets, including more companies seeking financing, increased investor activity, rising M&A actions, and a late-2023 surge in the Russell 2000. These signs suggest that growth-focused entities, like those in The Private Shares Fund, are poised for a strong 2024, anticipating interest rate cuts and a stable economy.

Despite ongoing market dislocations and excess inventory due to the private sector's structural challenges, for discerning investors, PSG sees enduring opportunities for beneficial deals through secondary transactions. The firm plans to continue its strategic investments, capitalizing on these conditions to achieve capital appreciation and successful exits for its investors, emphasizing the value of patience.

As of December 9, 2020, Liberty Street Advisors, Inc. became the adviser to the Fund. The Fund’s portfolio managers did not change. Effective April 30, 2021, the Fund changed its name from the “SharesPost 100 Fund” to “The Private Shares Fund.” Effective July 7, 2021, the Fund made changes to its investment strategy. In addition to directly investing in private companies, the Fund may also invest in private investments in public equity (“PIPEs”) where the issuer is a special purpose acquisition company (“SPAC”), and profit sharing agreements.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus with this and other information about The Private Shares Fund (the "Fund"), please download here, visit the Fund’s website at PrivateSharesFund.com or call 1-855-551-5510. Read the prospectus carefully before investing.

The investment minimums are $2,500 for the Class A Share and Class L Share, and $1,000,000 for the Institutional Share.

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. The Fund has no history of public trading and investors should not expect to sell shares other than through the Fund's repurchase policy regardless of how the Fund performs. The Fund does not intend to list its shares on any exchange and does not expect a secondary market to develop.

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund's outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund's investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund's investments will be valued by Liberty Street Advisors, Inc. (the "Investment Adviser") pursuant to fair valuation procedures and methodologies adopted by the Board of Trustees. While the Fund and the Investment Adviser will use good faith efforts to determine the fair value of the Fund's securities, value will be based on the parameters set forth by the prospectus. As a consequence, the value of the securities, and therefore the Fund's Net Asset Value (NAV), may vary.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund's quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund's expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices, such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities.

The Fund may invest in private securities utilizing special purpose vehicles ("SPV"s), private investment funds (“Private Funds”), private investments in public equity ("PIPE") transactions where the issuer is a special purpose acquisition company ("SPAC"), and profit sharing agreements. The Fund will bear its pro-rata portion of expenses on investments in SPVs, Private Funds, or similar investment structures and will have no direct claim against underlying portfolio companies. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund's risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. Investors are encouraged to consult with appropriate financial professionals before considering an investment in the Fund.

Companies that may be referenced are privately-held companies. Shares of these privately-held companies do not trade on any national securities exchange, and there is no guarantee that the shares of these companies will ever be traded on any national securities exchange

The Private Shares Fund is distributed by FORESIDE FUND SERVICES, LLC